You deserve financial advice you can trust.

At Guidance Financial Services, we don’t have our own investment products to promote, and our advice isn’t influenced by where your money is invested.

So, you can feel confident every recommendation is focused on what’s best for you.

The expert behind the Ask an Expert column

We believe financial advice should be accessable, clear, and free from conflict.

Financial advice shouldn’t be something only the ultra-wealthy can afford or understand.

We work with people at different stages of life, with different goals and different starting points. Our job is to help you understand your options, make better decisions, and feel more confident about where your money is taking you.

Whether you’re earning well but unsure if you’re on track, navigating a big life change, or just tired of second-guessing your decisions, we help you sort your finances, build your wealth and get clear on what to do next.

What’s brought you here?

(Choose the option that best fits your situation)

-

I want to make sure I’m set up for retirement

You want clarity on where you stand and what you should do next.

-

I’m in my 30s or 40s and want to get my finances set up properly

You’re earning well but want to make sure you’re actually on track.

-

I recently got an inheritance

You’ve been given a lump sum of money and want to make the right choice.

-

I’m going through a divorce or separation

You’re ready to rebuild and need a financial plan built for your new life.

-

My mortgage is paid off and I’ve got surplus cash

You want to make smarter decisions with your increased cash flow.

-

I want to set my kids up financially

You know you want to give them a head start, but aren’t sure what the smartest way to do it is.

What We Can Help With

-

Income & Cashflow

Make smarter decisions with the money coming in and going out. We help you understand your cashflow, manage competing priorities, and build a plan that gives your money a clear job.

-

Investment Strategy

We help you understand where to invest, how much risk makes sense, and how your investment plan fits into the life you actually want.

-

Retirement Planning

Get clear on when you can retire, how much you may need, and whether your money is on track to last. We help you plan for retirement so you can stop worrying about your future.

-

Superannuation

We help you make sense of your super, improve how it is structured, and use it properly as part of your long-term plan.

-

Personal Insurance

Protect the life you are building. We help you work out what cover you need, what you may not need, and how to make sure your insurance fits your income, family, debt and future plans.

-

Goal Setting

Turn vague money goals into a clear plan. We help you work out what you want your money to do, what needs to happen first, and how to keep each decision aligned with the goals you’re working towards.

-

Asset & Debt Strategy

Get a clearer picture of what you own, what you owe, and what to do next. We help you balance debt repayment, investing, property, super and cashflow so your money is working in the right direction.

-

Intergenerational Wealth

Make sure the wealth you build is passed on with care. We help you think through family, estate planning, tax, super and giving, so your money supports the people and causes that matter to you.

★★★★★

5 Star rating on Google

★★★★★ 5 Star rating on Google

What Our Clients Say

Get to know how we think

-

![Paul Benson and Nick Donato's money podcast Financial Autonomy]()

Financial Autonomy

PODCAST

-

![]()

Ask an Expert

WEEKLY NEWSPAPER COLUMN

-

![Reading Guidance Financial Services Money Newsletter]()

GainingCHOICE Newsletter

WEEKLY MONEY HEADLINES & INSIGHTS

-

![]()

Blog

UNDERSTAND YOUR FINANCES BETTER

-

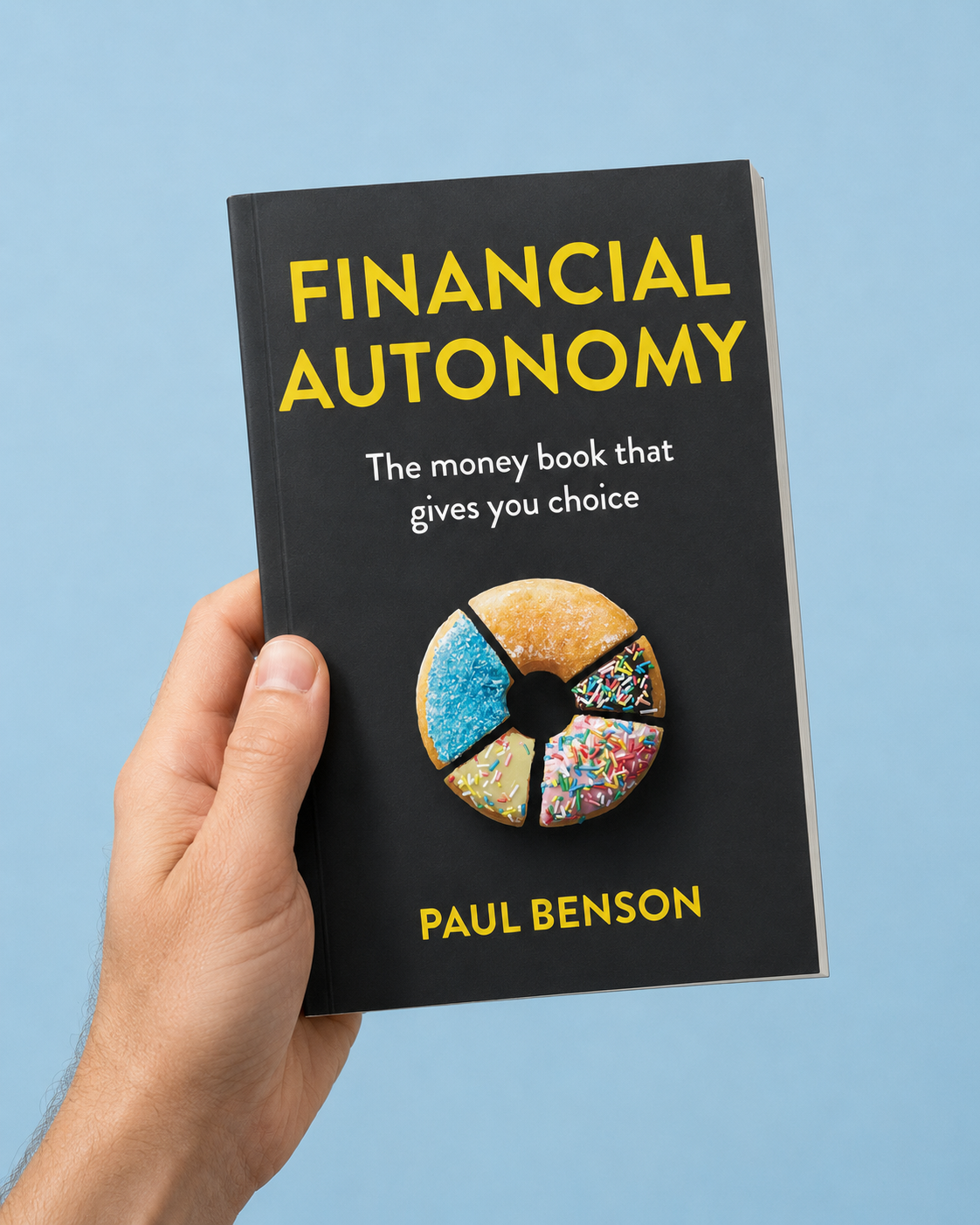

![]()

Financial Autonomy: The Money Book That Gives You Choice

BOOK

Read Our Articles

Frequently Asked Questions

Money decisions come with a lot of questions. Here are the ones we hear most often. If you still need clarity, you can contact us below.

-

When choosing a financial adviser, it's worth asking:

Do they manufacture their own products?

Do they earn more when you invest more?

We've structured our business so the answer to both is no — because advice should only ever be about you.

If trust has been one of the reasons you have delayed getting advice, we’re happy to answer any questions you have before you book to give you peace of mind.

-

Financial advice costs vary because everyone’s situation is different.

A simple question and a full financial plan are not the same thing.

The cost depends on what you need help with, how complex your finances are, and how much work is needed to build the right advice.

There are also some situations where your advice may be tax deductible or could be paid with your superannuation.What matters is that you understand the fee before you say yes.

As a guide, our advice preparation and implementation typically starts from $4,400, depending on what you need. A full financial plan with long-term projections usually ranges from $5,500 to $9,900.

For clients who want ongoing financial planning support, our annual service is renewed each year and typically ranges from $400 to $900 per month, depending on the size and complexity of your situation.

We are upfront about costs. We explain what the advice covers, what the process looks like, and what you can expect before you decide to move forward. -

You should see a financial adviser when the decision feels too important to guess.

That might be when you are planning for retirement, earning well but not feeling ahead, paying off your mortgage, deciding whether to invest, reviewing super, receiving an inheritance, going through divorce or separation, or trying to work out if you are actually on track.

A lot of people wait until they feel completely stuck. But the best time to get advice is often before the big decision is made, while you still have options.

At Guidance, we help you understand where you stand, what needs attention, and what steps could put you in a stronger position.

-

Because every year you wait is a year your super may be in the wrong structure, your cash could be working harder, and decisions get made by default rather than by design. The people who wish they'd done it sooner all say the same thing: the hardest part was starting.

-

Banks and super funds can give you information about their own products, but they can't give you advice that spans your whole financial picture. Wealth Builder covers cash flow, debt, super, investments, and protection together — because that's the only way to make sure everything is actually working in the same direction.

-

There is no one perfect super number. The amount you need depends on the retirement you want. A modest retirement, a comfortable retirement, and a retirement with regular travel are all very different numbers.

A good starting point is working out how much you want to spend each year, then looking at your super, investments, home ownership, retirement age, Age Pension eligibility, tax position, and how your money will be invested.

That is why generic super targets only take you so far.

At Guidance, we model your retirement properly. We can factor in things like travel, downsizing, selling assets, helping children, inheritances and tax, so you can see whether you are on track and what needs to happen next.

If you want retirement planning advice book an appointment with Guidance Financial Services here.

-

In most cases, yes. You want a clear plan to be debt free by retirement.

That does not always mean every spare dollar should go straight to the mortgage. Sometimes boosting super, investing outside super, or keeping cash available can also make sense.

But once you retire, mortgage repayments can put real pressure on your retirement income. Debt also reduces your flexibility, which matters because retirement does not always happen exactly when you planned.

The real question is not just should I pay off my mortgage? It is what is my plan for this mortgage?

At Guidance, we help you compare the options, including paying down debt, boosting super, investing, or using a mix of strategies, so you can work toward retirement with more clarity and fewer surprises.

If retirement is getting closer and you still have a mortgage, book a conversation with Guidance.

-

Probably not. But the sooner you look at it, the more options you usually have.

A lot of people avoid retirement planning because they are worried the answer will be bad. So they put it off, keep working, keep hoping, and tell themselves they will deal with it later. But “later” has a habit of becoming expensive.

If you are in your 50s or 60s, good advice can still make a real difference. You may be able to boost super, adjust your investment strategy, reduce debt, plan your retirement income, improve tax outcomes, or make smarter decisions about when and how you stop work.

At Guidance, we help you understand where you stand now, what gaps need attention, and what steps could put you in a stronger position from here.

-

Financial advice is not just for people close to retirement.

By the time retirement is around the corner, some of your best options may already be gone. The earlier you start, the more time you have to build wealth, reduce debt, grow your super, invest properly and fix the gaps before they become expensive.

In fact, research shows getting advice in your mid 30s could leave you more than $600,000 better off by retirement.

That is why we do not treat your 30s and 40s like a waiting room for “real” financial advice. We think this stage matters so much that we have a financial adviser dedicated to helping people in their their 30s and 40s, and we built a specialist program around it.

Our Wealth Builder program is designed specifically for people in their 30s and 40s who are earning decent money, but want to know they are actually making the most of it.

Wealth Builder helps you understand where you stand, what needs attention, and what to do next, so you can make the most of your peak earning years.If you are in your 30s or 40s and want advice built specifically for this stage of life, learn more about Wealth Builder here.

-

Extra super contributions can be powerful, but they are not automatically right for everyone.

Super can be tax effective, which is why it can be such a strong retirement planning tool. But the trade off is access. For most people, money in super generally cannot be accessed until at least age 60, and even then conditions apply.

So if you may need the money before then, investing outside super could be a better fit.

The right decision depends on your age, income, tax position, cash flow, retirement goals, debt, contribution limits and how much flexibility you need before retirement.

At Guidance, we help you work out whether extra super contributions fit your bigger plan, or whether your money may be better used elsewhere first.

If you want a financial plan that maximises the impact of your money, book an appointment with with Guidance Financial Services here.

-

At Guidance, this is the number one question we get from new clients, whether they are 20 years from retirement or six months out. And the answer is different for everyone, because it depends on your spending, retirement age, super balance, investment strategy, Age Pension eligibility, and what you actually want retirement to look like.

To answer it properly, we build a financial model that shows your expected long term trajectory. Then we use that as a baseline to test different options, like retiring earlier, working part time, increasing super contributions, downsizing, changing your investment strategy, or spending more in the early years while you are healthy enough to enjoy it

Because being on track is not just about having a certain amount in super.

It is about knowing whether your money can support the life you want, for as long as you need it to.

The real risk is finding out too late that your plan had a gap you could have fixed years earlier.

-

Yes, if the advice helps you make better decisions than you would have made on your own.

That is where good advice can make a serious difference.

A Findex worked example found that a woman earning $100,000 who started getting financial advice in her mid 30s could be $664,000 better off at retirement than if she never got advice. Waiting until age 50 reduced that gain to $192,000.

That is the point most people miss.

Financial advice is not just valuable because someone tells you where to invest. The bigger value often comes from the decisions that sit around the investment: contributing more to super, reducing tax where appropriate, choosing the right asset mix, avoiding panic decisions, consolidating super, protecting your income, and actually sticking to a plan.

At Guidance, that is exactly what we help you do and where the value of advice compounds.

-

Yes, but good investment advice is not about hot tips.

At Guidance, investing is part of the plan. We look at what your money needs to do, how much risk makes sense, when you need access to it, and how it fits with your super, tax, debt and retirement goals.

We focus on evidence-based investing and proper asset allocation. That means building a portfolio with the right mix of investments, rather than trying to guess which stock or fund will win next.

See more about how we invest here. -

This is one of the biggest questions people ask, especially in their 30s, 40s and 50s. And the honest answer is: it depends.

Paying down the mortgage can give you security and reduce stress. Investing can help you build wealth over time.

The right answer depends on your income, interest rate, age, tax position, super balance, goals, risk tolerance and timeline.

This is where guessing can get expensive.

At Guidance, we model the options so you can see what each path may mean before you commit.

If you are stuck between mortgage, super and investing, book a conversation. This is exactly the kind questions we answer.

-

First, celebrate. Paying off the mortgage is a big deal. Then make a plan.

Once the home loan is gone, you may suddenly have more cash flow. The question is what that money should do next.

At Guidance, we help you decide how to use that surplus cash in a way that strengthens your future, instead of letting it quietly disappear into lifestyle creep.

If your mortgage is paid off and you are asking what now, this is a perfect time to get advice. You can book your appointment here.

-

Accountants and financial advisers do different jobs. Your accountant usually helps with tax returns, business structures and compliance.

A financial adviser helps you plan what to do with your money. That includes super, investing, retirement, insurance, debt, cash flow and long term strategy.

You may need both, especially if your decisions affect tax and your future.

At Guidance, we can work alongside your accountant where needed, so your tax position and financial plan are considered together.

-

A mortgage broker helps you get a loan. A financial adviser helps you work out how that loan fits into your life.

A broker might help you refinance. An adviser helps you decide whether to pay extra into the mortgage, invest, add to super, keep cash aside or change your broader strategy.

Both can be useful. They just solve different problems.

We also have mortgage brokers we can refer you to. -

Yes. Guidance Financial Services is based in Essendon, Melbourne, but we work with clients across Australia.

All of our meetings can be done online, making it easy for you if you can’t make it into our office.

-

No. While our office is based in Essendon, Melbourne, we provide financial advice to clients across Australia. We work with people in Melbourne, Sydney, regional Victoria, New South Wales and other locations through online appointments.